Form 6765 Instructions

Form 6765 is used to claim the federal Research and Development tax credit. You can file it if your business performs qualified research activities and incurs qualifying expenses such as wages, supplies, and contract research.

The form now includes new Sections E, F, and G, updated election rules under Section 280C, new naming conventions for attachments, and updated guidance for controlled groups. To file correctly, calculate your credit using both Regular and ASC methods, document all research activities, confirm you qualify as a small business if electing the payroll credit, and complete Sections A through G based on your structure and activity.

.png)

The R and D credit rewards businesses that invest in innovation. Form 6765 provides the framework for calculating the credit, electing reduced credit treatment, and optionally applying up to 500,000 dollars of the credit against employer payroll taxes. The updated 2025 instructions affect how taxpayers document their Qualified Research Expenses, claim elections, and file attachments. Filing correctly can reduce tax liability significantly, but requires accurate documentation, correct method selection, and awareness of new IRS requirements.

What Is Form 6765

Form 6765 instructions, Credit for Increasing Research Activities, is used to calculate and claim the federal R and D tax credit. It applies to any business that incurs Qualified Research Expenses related to developing new or improved products, processes, software, or technologies. The form also allows small businesses to elect the payroll tax credit option and lets filers elect reduced credit treatment under Section 280C.

What’s New in 2025 Form 6765 Instructions

Section 280C Election Moved to Item A

Taxpayers now elect the reduced credit at the top of Form 6765. You must choose Yes or No on your original filed return. Amended returns cannot modify this election.

Controlled Group Disclosure Added to Item B

Item B asks whether your business is part of a controlled group or under common control. If Yes, you must attach a detailed statement using the IRS naming convention.

Section E Introduced for Additional QRE Information

This new section expands disclosure requirements for Qualified Research Expenses. Line 48 requires supporting details.

ASC 730 Directive Clarification in Line 41

Taxpayers using the ASC 730 directive must select Yes or No.

Sections F and G Added

Section F summarizes QRE totals to determine whether Section G is required.

Section G requires detailed business component information but is optional for tax years beginning before 2025 unless filing an amended return.

Updated Naming Conventions for Attachments

Electronic filers must follow specific naming rules when submitting attachments.

Who Must File Form 6765

You must file Form 6765 if your company:

- Performs qualified research

- Incurred Qualified Research Expenses

- Wants to claim the R and D credit

- Is a small business electing payroll credit treatment

- Is part of a controlled group with shared research activity

Partnerships and S corporations must file Form 6765 at the entity level. Estates and trusts may allocate credits to beneficiaries.

What Counts as Qualified Research Activities

To qualify, research must meet the IRS four part test:

- Permitted Purpose

Improving function, performance, quality, reliability, or cost efficiency. - Eliminating Technical Uncertainty

The activity must address uncertainty about capability, methodology, or design. - Technological in Nature

The research must rely on hard sciences—engineering, computer science, biology, chemistry, or physics. - Process of Experimentation

The activity must involve evaluating alternatives through modeling, testing, simulation, prototyping, or trial and error.

Activities That Do Not Qualify

- Market research

- Consumer surveys

- Website content creation

- Reverse engineering without improvement

- Foreign research

- Routine data collection

- Ordinary quality control

- Post production testing

Documentation Checklist for R and D Credit Claims

Businesses should gather:

- Project descriptions

- Engineering notes

- Technical requirements

- Design documents

- Code repositories

- Flowcharts

- Lab reports

- Employee time allocation

- Contracts for subcontracted R and D

- Expense reports

- Prototypes or testing results

Poor documentation is a major cause of rejected credit claims.

Qualified Research Expenses Explained

Wages

Include wages, bonuses, stock based compensation, and payroll taxes for employees who:

- Directly conduct research

- Supervise research

- Support research efforts

Supplies

Tangible non depreciable property consumed in the research process.

Contract Research

65 percent of payments made to third party contractors for research.

Section by Section Instructions

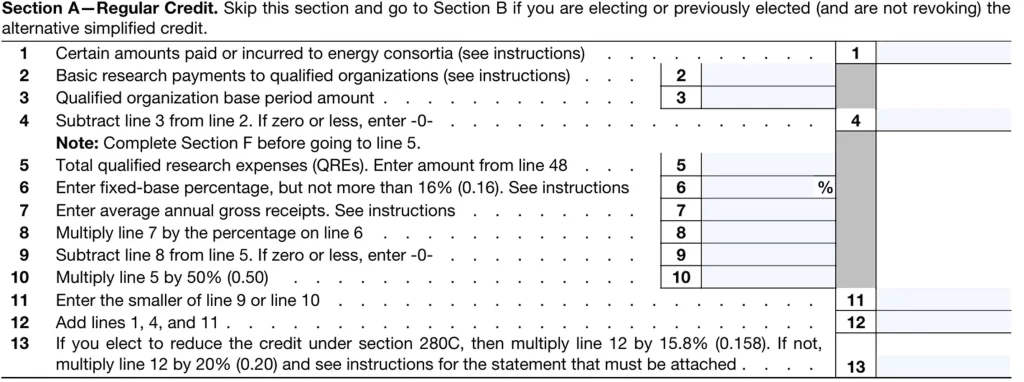

Section A: Regular Credit Calculation

Calculates credit as 20 percent of the increase above your base amount. Best for companies with consistent research history.

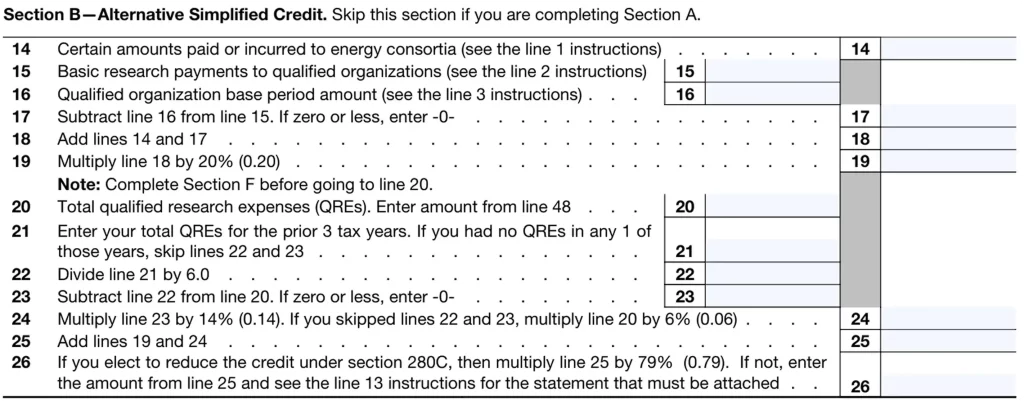

Section B: Alternative Simplified Credit (ASC)

Calculates credit as 14 percent of the difference between current QREs and 50 percent of the average QREs from the prior three years.

Section C: Current Year Credit Information

Summarizes your total credit and breaks it down by entity type where applicable.

Section D: Payroll Tax Credit Election for Small Businesses

Small businesses can apply up to 500,000 dollars of credit against employer Social Security and Medicare tax.

Must meet:

- Less than 5 million dollars in current year gross receipts

- No gross receipts prior to the previous 5 years

Section E: Other Information

Newly added. Requires detail on QRE composition.

Section F: Qualified Research Expense Summary

Determines whether Section G is required.

Section G: Business Component Information

Requires disclosure of business components generating the research. Optional before 2025 unless filing amended returns.

How to File Form 6765 Step by Step

- Confirm Eligibility Using the Four Part Test

Ensure your work meets IRS requirements. - Gather QRE Documentation

Collect wage data, contractor invoices, supply expenses, and technical documents. - Calculate QRE Totals

Organize all expenses by category. - Compute Credit Using Both Methods

Run Regular and ASC calculations and select the larger credit. - Decide Whether to Elect the Section 280C Reduced Credit

Choosing Yes simplifies tax reporting but reduces the credit by 21 percent. - Determine Whether You Qualify as a Small Business

If yes, complete the payroll tax election. - Complete Sections A to G Based on Your Activity

Follow the updated 2025 instructions. - Attach Required Statements

Controlled groups and amended returns require formal attachments. - File With Your Tax Return

Include Form 6765 with your corporate, partnership, or individual tax filing.

Payroll Tax Credit for Startups

Startups can apply up to 500,000 dollars of credit per year to payroll liability. The credit applies after filing Form 6765, and is claimed using Form 8974 in quarterly payroll filings.

Controlled Group Rules

Controlled groups share research expenses and credit limitations. Groups must aggregate QREs and calculate one credit, which is then allocated based on expenses incurred.

BooksMerge Insight

Our analysis of more than 1,000 small businesses and startups between 2021 and 2024 shows that most companies lose R and D credit value not because they lack qualifying research, but because they track it too late. Roughly 47% of businesses start gathering documentation only at tax time, which reduces allowable QREs by an average of 15% to 22% . Companies that track project activity and employee time quarterly instead of annually captured 28% more qualified expenses and saw a 35% higher approval rate with the IRS. Consistent recordkeeping, not larger research budgets, is what creates stronger and more defensible Form 6765 filings.

Common Errors to Avoid

- Ignoring required attachments for controlled groups

- Not calculating both Regular and ASC credits

- Missing Section 280C election

- Failing to document experimentation steps

- Incorrect wage allocations

- Claiming non technical work as QREs

- Filing amended returns without meeting new Section G rules

Penalties and Risks

The IRS may reject claims that lack documentation. Large inaccuracies may lead to penalties, interest, or additional tax assessments.

FAQs

1. Is software development eligible for the credit?

Yes, if it meets the four part test.

2. Can I claim credit for research outside the United States?

No.

3. Is Section G required for all filers?

Optional until 2025 unless filing an amended return.

4. Can startups claim the payroll election multiple years?

Yes, until the 500,000 dollar annual cap is reached.

Conclusion

Form 6765 provides significant tax savings to companies that innovate. Understanding the updated 2025 instructions, correctly documenting research activity, and selecting the best calculation method can increase your credit and protect your business during IRS review. If you need professional support, BooksMerge experts can help you prepare documentation, verify eligibility, and file Form 6765 accurately.